How does the financing of a circular business model work

Three types of financing

In general, funding is available in the form of participations, loans or public funding. The right type of financing depends on circumstances such as the type of circular business model and the development phase of the organisation.

Participation (equity)

In a participation, capital is provided in exchange for a participation in the company (part of the ownership). Participation is therefore a form of equity. An example is venture capital financing for an unproven and untested cradle-to-cradle technology. In particular, start-ups in the Netherlands are hampered by a lack of this type of risk capital. Oliver Wyman has estimated that €400-500 million in venture capital will be needed until 2022 to get the circular economy off the ground (Oliver Wyman, 2017).

Loans (debt)

Debt financing is provided in the form of a loan that is repaid in instalments or in full, including interest, at an agreed time. This means that the company enters into a debt, which is also referred to as loan capital. Examples are:

· Crowdfunding: through crowdfunding platforms, entrepreneurs can finance their plans through a large group of private investors, for example through OnePlanetCrowd, where more than € 50 million has been invested in sustainable projects since its establishment.

· Leasing finance: e.g. leasing light on a pay-per-lux basis between Philips and Rau Architects or leasing furniture by C2C ExpoLab;

· Impact loan: financiers such as Rabobank offer loans with an interest rate discount to companies whose products or services have a positive social or environmental impact.

Public funding

The government has various policy instruments at its disposal that can (financially) support the transition to the circular economy. This can be done through indirect financing, such as fiscal instruments, subsidies or purchasing policy, but also through direct financing (Van Tilburg, Achterberg and Boot, 2018):

· Guarantees: Through a guarantee, the government covers (part of) the financial risk of a financing (loan or equity).

· Loans: The government can also provide loans itself. For example, an innovation credit, a loan that is waived if the project fails. This can be an effective instrument to stimulate R&D.

· Participations: The government can also become the (partial) owner of a company itself. This is mainly done in sectors or projects that are of general interest, but which are not provided for by the market.

The right funding for the right situation

Each circular business model has its own risk profile. This requires different forms of capital. Young and fast-growing companies in particular are dependent on external financing. This financing can take the form of participations or loans (see the previous section). Crowdfunding can be a suitable source of financing if the business model has a strong community aspect. Various forms of capital will have to be mobilised to finance the transition to the circular economy.

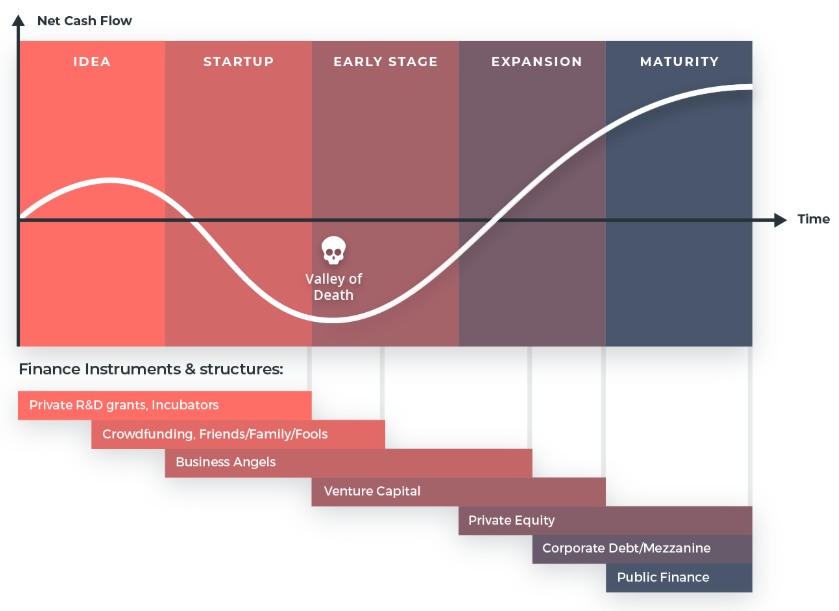

It is important for a company to determine which form of financing best suits its needs. This need largely depends on the phase in which the company finds itself. The figure below compares the net cash flow with the company’s growth phase. Usually, a company’s greatest financial needs arise when they try to overcome the so-called ‘Valley of Death’. This is the period between receiving seed capital (start-up) and the moment when the company starts to generate profits.

Figure 1: Financial instruments and structures (Achterberg and Van Tilburg, 2016).

In general, most funding barriers are experienced in the early stages of a company’s existence because of the high degree of uncertainty. In the idea and start-up phase, there is technological risk: the uncertainty as to whether the product or idea will work technically. If the company’s technology is proven to be effective, the company moves to the commercialisation phase where mainly market risk plays a role: the uncertainty of whether there will be sufficient market demand for the product or service. This risk occurs during the later start-up phase, the so-called early stage and the beginning of the expansion phase. Finally, during the expansion and maturity phase, there is the execution risk in which a company has to scale up. Different phases therefore have different risk profiles and therefore require different financial instruments, which are summarised in Figure 1.